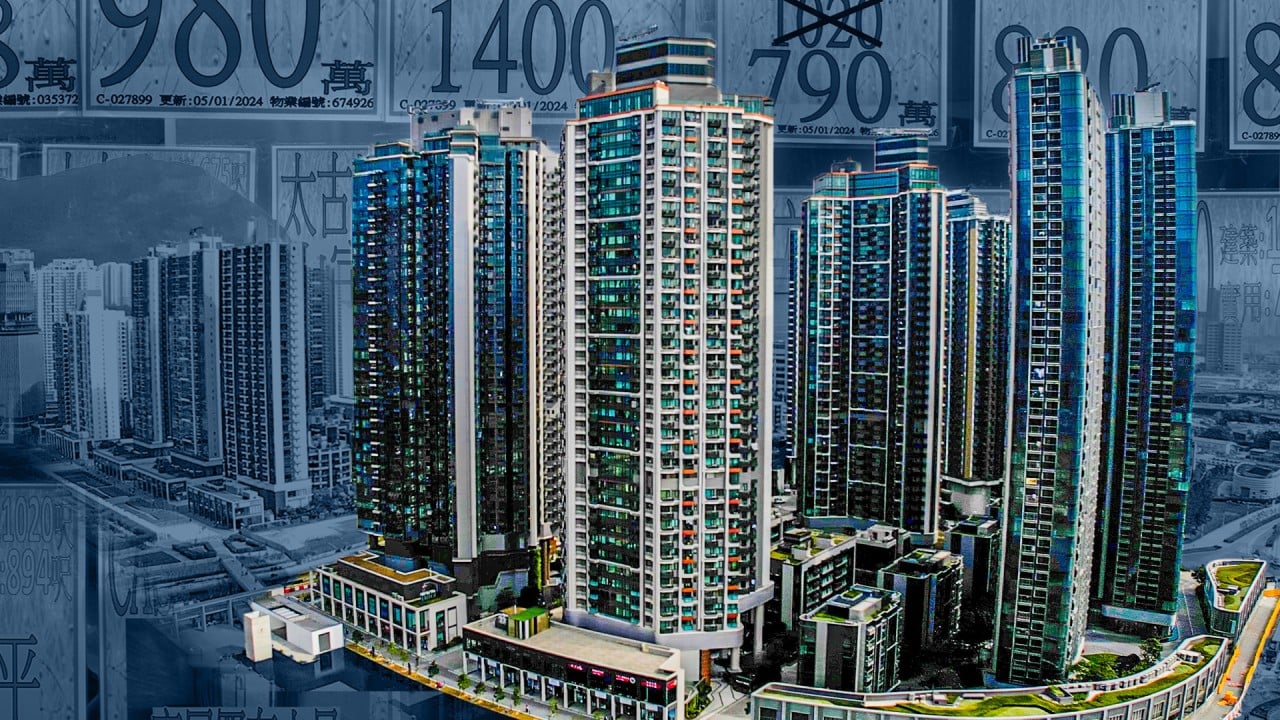

Residential buildings seen from a scenic overlook in Hong Kong on February 25. The lifting of cooling measures in the property sector after more than a decade has sparked a surge of home purchases among local buyers and those from mainland China. Photo: Bloomberg

Opinion

The View

by Nicholas Spiro

The View

by Nicholas Spiro

Ending cooling measures no game changer for Hong Kong property market

The end of more than a decade of cooling measures for Hong Kong’s property market is welcome and has sparked a surge in new home sales

These changes must be put in proper context, though, as several other factors will be more consequential in setting the property sector’s course

If there is a real estate market in Asia that deserved some good news, it is Hong Kong’s. On February 28, the city’s Financial Secretary Paul Chan Mo-po and Hong Kong Monetary Authority chief executive Eddie Yue Wai-man lifted the spirits of the residential sector by announcing that long-standing cooling measures would be scrapped and macroprudential regulations in the mortgage market would be eased.

Having suffered a nearly 25 per cent decline in secondary prices since the September 2021 peak and a drop in sales last year to a 33-year low, the city’s housing market has been given a much-needed shot in the arm. Additional stamp duties for non-permanent residents, those purchasing a second property and those reselling their homes within two years were abolished with immediate effect.

Hong Kong’s de facto central bank also suspended the interest rate stress-testing requirement for mortgage loans and allowed buyers to borrow more to purchase more expensive properties.

The impact of the changes is already palpable. New home sales surged to 117 in the first five days following the policy shift, compared with an average of just 11 in the two months before the announcement, according to data from Midland Realty.

Morgan Stanley has turned bullish on the city’s housing market. In a report published just after the changes were introduced, it said the total addressable market of potential new buyers had increased sharply.

In addition to mainland Chinese buyers and non-permanent residents, 408,000 citizens and permanent residents have assets greater than HK$10 million (US$1.3 million) and could buy a second home as an investment, while the 66 per cent of households that are mortgage-free could take out a mortgage.

Having forecast a 10 per cent drop in house prices this year before the measures were announced, Morgan Stanley believes the policy shift will lead to a 5 per cent rise. “We believe it’s a big deal,” said Praveen Choudhary, managing director and head of Hong Kong and India real estate research at Morgan Stanley, who predicts the market has finally bottomed.

This could well be the case. The removal of the restrictions will draw in more buyers, helping front-load some of the demand from those waiting to obtain permanent residency and providing an incentive for some residents to upgrade or buy a second property for investment purposes. Moreover, the policy shift comes at a critical time in Hong Kong’s efforts to bolster its appeal relative to regional rival Singapore.

In April last year, Singapore doubled additional stamp duties for foreigners buying a residential property to a staggering 60 per cent amid fears over an influx of Chinese money pouring into its market because of its safe-haven appeal.

Hong Kong’s decision to scrap additional stamp duties for foreigners makes Singapore’s tightening measures look even more draconian. The International Monetary Fund said it “did not find evidence” that would justify such a punitive and discriminatory levy. This is not surprising given that Singaporean citizens and permanent residents account for the majority of demand for private properties.

Hong Kong’s cooling measures, which were introduced more than a decade ago, also had their limitations. S&P Global Ratings notes that while transactions in the secondary market fell sharply after levies were imposed on those reselling their properties within three years, the steep decline in monthly turnover “drove prices higher, to a certain extent”.

Other factors, notably severely constrained supply and low mortgage rates, were more important. This only goes to prove that scrapping the cooling measures is not a game changer for the city’s housing market.

13:00

How Hong Kong's housing market became among the world’s most unaffordable

How Hong Kong's housing market became among the world’s most unaffordable

For starters, mortgage rates have risen sharply and are higher than rental yields, resulting in a “negative carry” that suppresses demand. Although expectations are building that the US Federal Reserve will start cutting interest rates later this year, the outlook for monetary policy remains uncertain.

Second, according to JPMorgan, the inventory of completed but unsold private new homes has risen to an all-time high, with additional supply putting further pressure on the market. S&P Global Ratings notes that even if demand in the primary market recovers to its recent high of 21,000 units in 2019, supply during the next three to four years will exceed demand.

Third, Hong Kong’s economy and markets have been hit hard by China’s cyclical and structural downturn. The Hang Seng Index – which is positively correlated to home values – has nearly halved since its peak in February 2021. Once a source of resilience, China’s economy is now the main threat to Hong Kong asset prices.

A pedestrian passes an electronic sign showing the Hang Seng Index in Hong Kong on February 28. Photo: AFP

Increasing volatility in Hong Kong’s property values during the past decade strengthens the case for establishing boundaries between the private and public housing markets.

Ryan Ip, vice-president and co-head of research at Our Hong Kong Foundation, said he believes the government should create a separate housing market for permanent residents comprising subsidised flats that would be sold only to those with permanent residency.

While the private market would remain unchanged, open to everyone including foreigners and investors, permanent residents would be shielded from excessive price swings. “The idea isn’t novel. Singapore’s public housing system is ring-fenced from the private market as only citizens and permanent residents are eligible to buy [subsidised] flats,” Ip said.

Hong Kong is not Singapore, especially when it comes to the housing market, which in the city state’s case is dominated by the public system. Yet this underscores the need to put Hong Kong’s cooling measures into context. Other factors – the supply-demand balance, interest rates, affordability and geopolitics – are more consequential.