Ukraine crisis: why investors should fear inflation and interest rate rises, not war

- Geopolitical tensions are not always bad for stock markets, which have a history of going up in times of conflict

- Inflation, higher interest rates and reductions in central bank liquidity will do more damage to economies than a territorial war in Ukraine

The Japan team – the only office awake at that time around the world – were in the morning meeting and didn’t immediately get the message. This was in prehistoric, pre-email times. A secretary put a message slip on the boss’ desk. Another secretary came along five minutes later and put a piece of paper on top of the first, and so on.

Just before lunch, the team leader finally got to the bottom of the pile to see the message, but by then the whole world knew. He said that if he had got the message on time, he would have sold. In fact, the Hong Kong market was up more than 40 per cent by the end of the year, so he should have bought.

Nathaniel Rothschild knew something about wars. During the Napoleonic wars, he reportedly coined the phrase, “buy to the sound of cannons, sell to the sound of trumpets”. It was as accurate in 1991 as it was in 1812, when Napoleon Bonaparte advanced on Russia.

However, Rothschild also benefited from the trumpets. To protect his real business of transporting gold to pay the troops, he had a communications system of messengers, horses, carrier pigeons and fast boats at the ready.

He was first with the news in 1815 that the Duke of Wellington had been victorious at the Battle of Waterloo, beating the official messenger. The story goes that no one in London believed him, so he took advantage and made a killing on the stock market.

Information is power – it just depends on what you do with it. Geopolitical squabbles can have an unpredictable influence on markets as the shocks and outcomes can be completely binary. Even Wellington reportedly described his victory at Waterloo as a “close-run thing”.

Today’s leaders have not experienced the horrors of all-out war. Even if they disregard the catastrophic effect on their own people, they know that there is no winner in direct superpower conflict.

02:27

Amid Russian troop build-up in Belarus, Ukrainian soldiers doubt good result in Kremlin-US talks

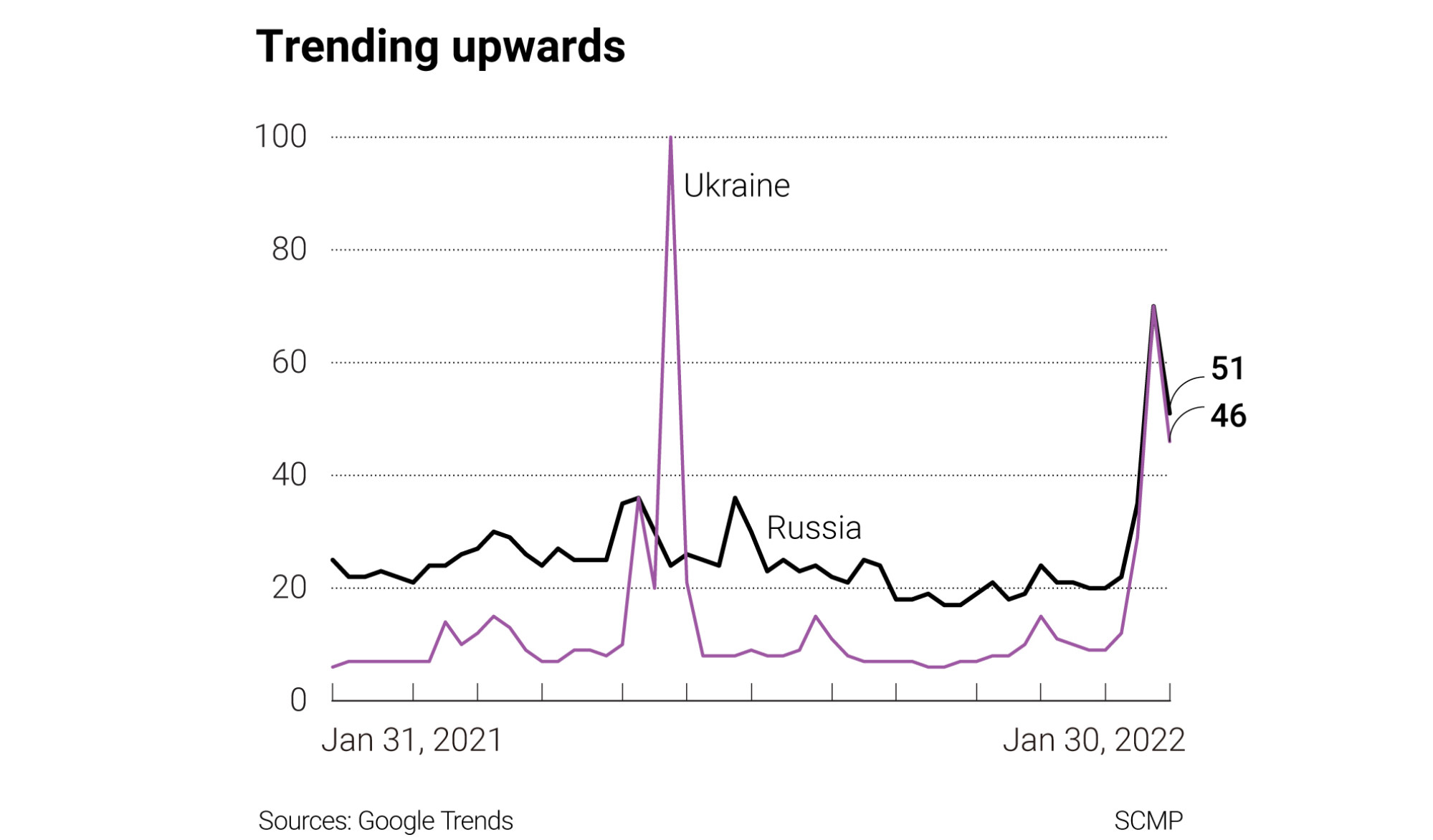

The narrative indicates high tensions in Ukraine, but it is just a localised spike in levels that are the highest since the Cold War. Yet, tension is not always bad for stock markets. Prices might show great volatility as the news story progresses, but markets regularly go up in times of conflict.

Investors cannot invest just for the worst-case scenario because, by definition, it is one of the least likely outcomes. Rampant inflation, the debasement of money, the raising of interest rates and the reduction in central bank liquidity will do far more damage to economies than a territorial war in Ukraine.

Nevertheless, even though equities are expensive, liquidity is still high, the US Federal Reserve still has the will and the firepower to support markets, and early-stage inflation is more likely in the short term to assist companies rather than damage them. But it is a close-run thing.

Richard Harris is chief executive of Port Shelter Investment and is a veteran investment manager, banker, writer and broadcaster, and financial expert witness