China’s property policy ‘arrows’ set to rescue developers, but with buyers’ faith shaken, will boom times return soon?

- The policy ‘arrows’ Beijing fired in November will aid developers, but observers differ on the timing and magnitude of a rebound for the US$2.55 trillion market

- Faith in price appreciation has been shaken, and demographics do not favour a return to the boom conditions of the last two decades, some analysts say

Four years ago in Shenzhen’s Nanshan district, home to the headquarters of tech giants Tencent and Baidu, nearly 1,000 applicants braved long queues in hot weather for a chance to buy one of 167 flats.

Each hopeful had deposited 5 million yuan (US$715,000) to participate in the city’s first public housing lottery – a scheme specially designed for situations where demand from interested buyers far exceeded supply.

Some of the would-be buyers stopped at temples to pray before joining the queue, and some brought lucky coins. The line included a cross-section of society, from children in strollers to elders using canes, with individuals and families hoping to buy flats priced at 140,000 yuan per square metre.

Today in the same neighbourhood, the queues are gone, and surplus homes abound. The One Bay development by state-backed Tagen Group recently managed to woo only 387 buyers for 416 units on offer, despite an average price of 96,000 yuan per square metre.

“You cannot imagine how poor sales are in other cities in China if the hottest market dipped into a freeze like this,” said Tommy Wu, senior China economist with Commerzbank.

In November, the central government emphatically stepped in to support beleaguered developers in an attempt to arrest the market’s free fall. This has led optimists to expect the quick resumption of a two-decade boom that saw the housing market grow into a US$2.55 trillion engine of China’s economic growth. However, analysts warn that the rebound may be slow to gather steam. And some even believe that the boom times are gone for good amid shattered consumer confidence and changing demographics.

“The property sector is a big drag on GDP growth [this year],” said Wang Tao, chief China economist with UBS, who estimates that the industry’s downturn sliced three percentage points off 2022 expansion.

Now observers hope the property sector – teetering on piles of unpaid debts, unfinished homes and stagnant sales – can bottom out sometime next year with support from the central government’s rescue measures.

Given China’s relaxation of Covid restrictions UBS’s Wang believes the market should see some recovery from the second quarter of next year onwards.

Real estate will only deliver a marginal contribution to the country’s GDP – about one tenth – a huge scaling down from the current level of one third, the economist said.

“It will not be such a big drag [on the economy] any more, but it will also not be a major engine of growth,” she said.

Residential housing construction has become one of the main pillars of China’s extraordinary growth in the past few decades. Homes were a communal right during Mao Zedong’s era, and private housing ownership was first fancied by Deng Xiaoping in late 1980s. The private market scaled up nationally under Jiang Zemin starting in 1998.

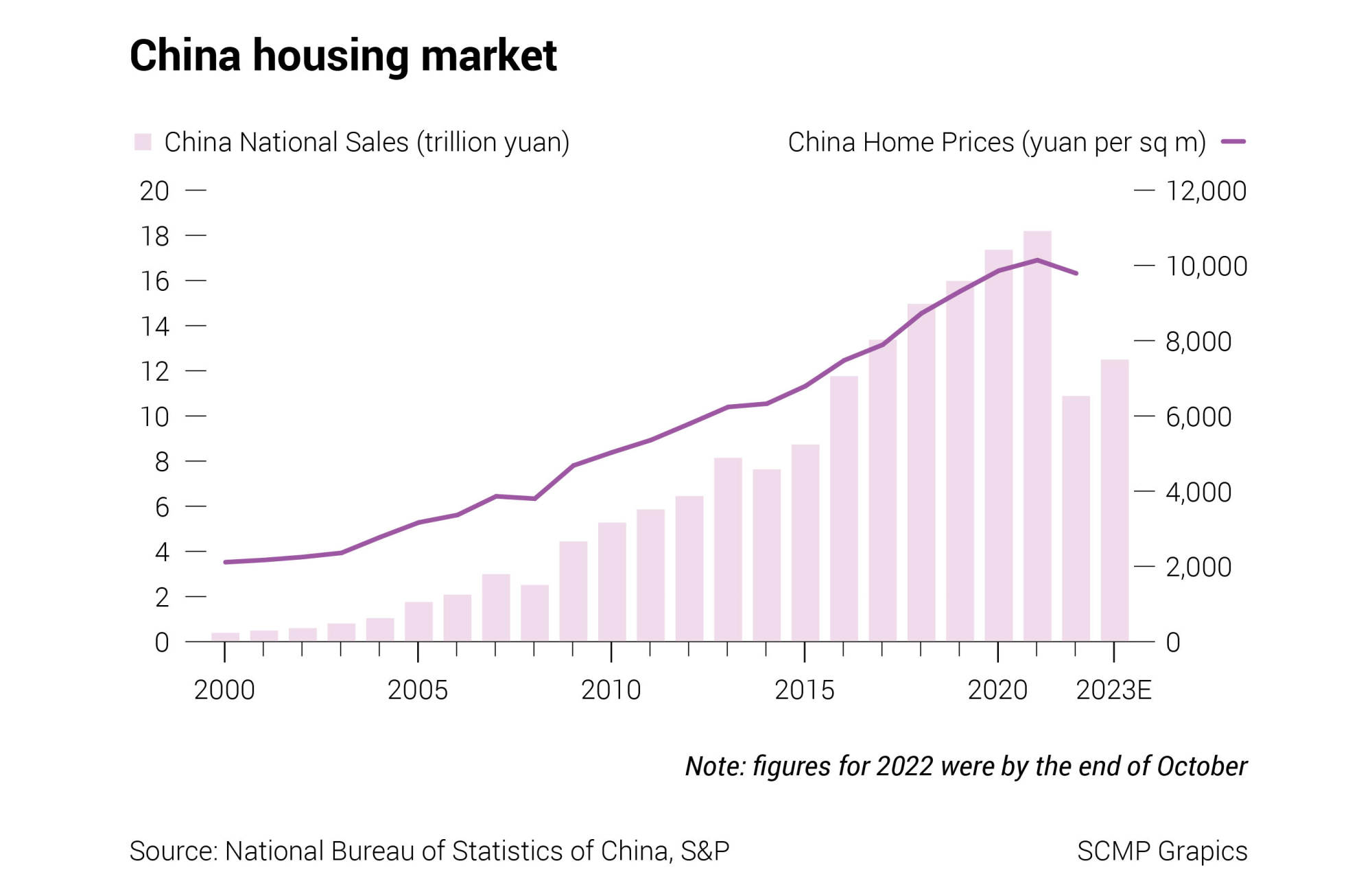

New home sales grew almost every year in the 2000s on their way to the US$2.55 trillion peak in 2021, which was slightly higher than total transactions in the US last year. The only exceptions were relatively small dips in 2008 due to the financial crisis and a setback in 2014 as China fought against overcapacity.

The current retreat, analysts agree, will be larger and longer.

As of the end of October, Chinese buyers bought 10.8 trillion yuan worth of new homes this year, falling more than 25 per cent short of the same period in 2021.

“If all the favouring policies are implemented promptly, this will stop the downward spiral, and surely can boost financing for developers,” said Lawrence Lu, S&P Global Ratings’ senior director. “But the sales will remain very weak due to economic slowdown, Covid control policies and, most of all, the heavily damaged confidence of homebuyers in China.”

S&P expects new home sales to finish 2022 at 13 trillion yuan, down 28 per cent year on year, and forecasts a further decline to 12.5 trillion yuan in 2023.

“The golden era where long queues and lucky draws were needed for home sales is gone, and I do not see that there is a way of it coming back,” said Michael Zhang, a veteran property agent in Zhongshan, in Guangdong province. Zhang has not brokered a single deal, new or lived-in, in November, and managed only three in October.

A property agent for 11 years, Zhang recalls bringing in a record 21 deals in the month of September 2018, when Zhongshan was first named as one of the cities in the new Greater Bay Area concept outlined by President Xi Jinping. At the time, home seekers from Macau, Hong Kong and Shenzhen were coming to the city in organised house-shopping groups.

“Now sales centres are full of discounts and promotion gimmicks,” Zhang said. “But none of these are luring them back. After all, why do you want to buy something that you expect to become cheaper?”

Owning a home is a nearly universal desire. Prices that have skyrocketed 380 per cent in the past two decades encouraged Chinese people to believe that home ownership was also the quickest, safest way to get rich. A 2015 stock market meltdown that destroyed US$5 trillion in wealth only reinforced the belief.

But now tumbling prices may bring that faith to an end.

House prices stood at 9,789 yuan per square metre on average at the end of October, down 3.5 per cent from 10,139 yuan per square metre at the end of 2021. Considering developers are still offering discounts to woo buyers, prices are very unlikely to rise.

In other words, China will see its first price crunch for homes in more than a decade.

That translates to paper losses for homebuyers who bought in the past couple of years. But for Zeng Xiaolu, a distressed home auction broker, it translates to more business.

“Recently, it is not possible to find a buyer without a sharp discount as people are expecting home prices will continue to fall,” Zeng said. “Thus, people who had debts to clear would just choose to give up their homes to the creditors through distressed auctions.”

Zeng expects his business to double by the end of next year.

“In rosy days, people who need money at short notice can always dump their homes on the secondary market quickly for a rather decent price,” he said. “But it is a different market now.”

Bank of America (BofA) sees “more reasons that prices will come down in the near future” while S&P expects that while major cities will remain very stable, small cities will see a 10 to 15 per cent drop through 2023.

“By the time that there is a consensus for property prices to go down, this usually becomes a downward spiral,” said Helen Qiao, chief Greater China economist and head of Asia economics at BofA Securities. “We think that it is hard to turn around the sentiment right away, for people to think that it will go up again.”

Reining in prices was a key purpose of China’s crackdown on the real estate market in the last few years, with all the cooling measures including the three red lines policy that limited developer borrowing. Rising prices were dubbed unfair and a cause for anxiety for Chinese people.

Now, as an era of falling home prices ensues, other issues emerge.

Chinese citizens devote as much as 69 per cent of their savings toward housing, roughly double the 35 per cent in the US, according to figures compiled by economist Ren Zeping, formerly of the Development Research Center, this May.

Sinking home prices mean a decline in their wealth, which brings trepidation and discourages consumption, the key driver of GDP.

“When you see your assets worth less money, you will spend less,” said Meng Xiaosu, who spearheaded China’s property reform policies in the 1990s as the head of a housing reform research group. “How is that good for the economy?”

Known as China’s “godfather of real estate”, Meng was president of China’s first property firm, the China National Real Estate Development Group (CNRED), and is now chairman of Huili Fund, an asset-management firm.

He believes that it is time for China to revisit its housing market playbook.

“High prices of private homes are not to blame,” he said. “The problem is that we do not have enough affordable homes.”

China has some 80 million government-subsidised affordable homes, and is adding another 1.8 million annually between 2021 and 2025, according to the housing authority.

However, the private-home market has 400 million homes across the country and another 10 to 18 million a year in the pipeline.

“For a very long time, we only focused on the private home market and left the affordable homes off the radar,” said Meng. “It is a critical time for the country to better establish a two-track system, as we first proposed when shifting to private home ownership in the 1990s. The state-owned property companies should take the responsibility to focus on this area.”

Fundamental demographic changes in China also argue against the return of an ever-booming housing market.

China will need only 10 million new flats a year by 2035, about half the number sold in the nation last year, according to US investment bank Goldman Sachs.

“China’s population growth has slowed, and we would expect to see less need for home construction going forward,” said Andrew Tilton, chief economist for Asia-Pacific with Goldman Sachs. “So regardless of what policymakers do, the need for constructing new housing would be going down over time.”