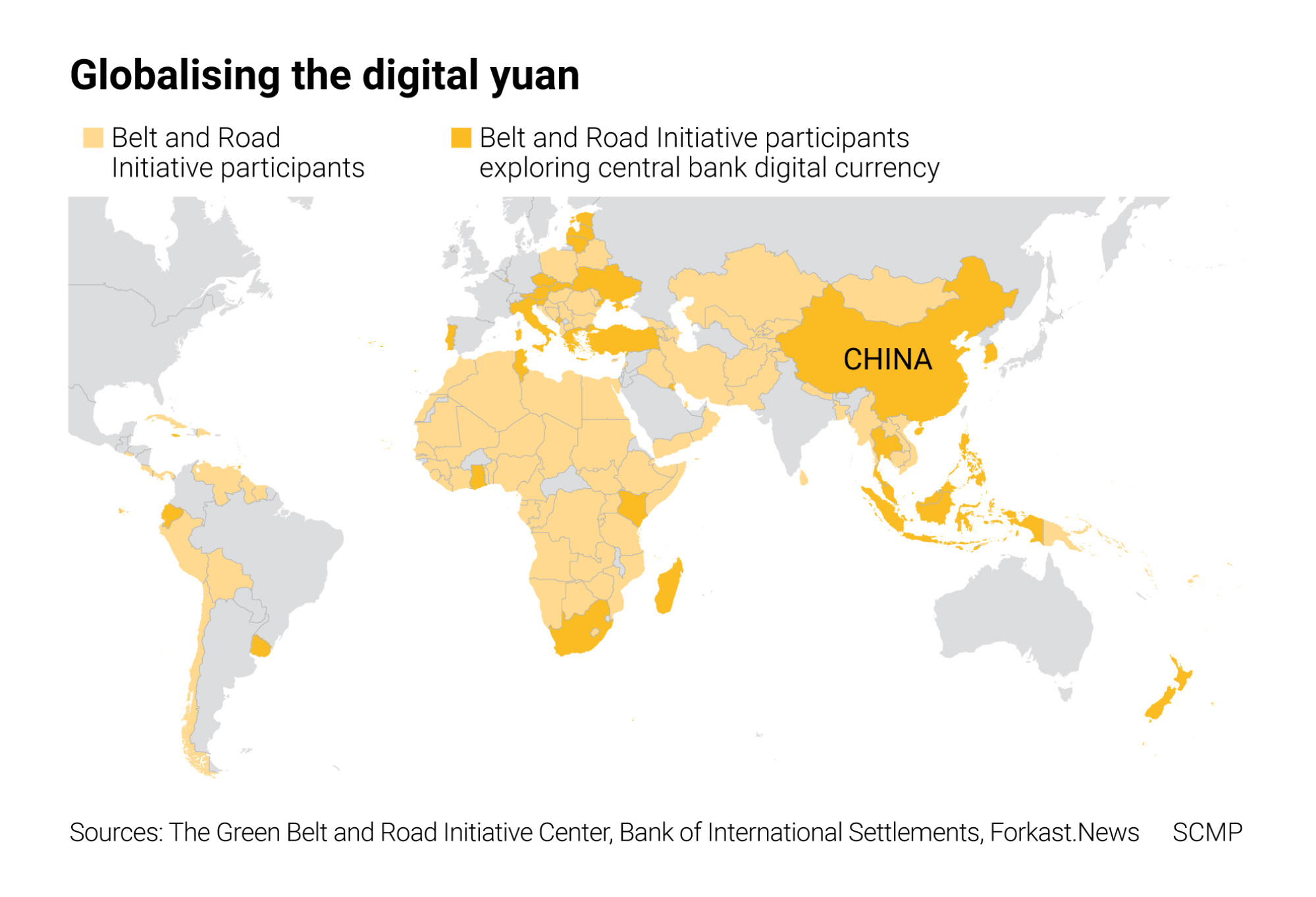

Where bitcoin fails, central bank digital currencies will succeed

- The restricted use and security risks of bitcoin and other cryptocurrencies make them a poor alternative to traditional currencies, even if they could overcome widespread official disapproval

- Central bank digital currencies, on the other hand, can help speed up transactions, reduce costs and improve security

Advocates of bitcoin and other cryptocurrencies argue that traditional fiat currencies are inherently unstable and that the monetary systems that underpin them are inefficient and corrupt. Yet the argument that bitcoin provides a more stable alternative is not playing out very convincingly in real time.

Against the dollar, bitcoin has traded in the range of US$30,000 to US$64,000 this year. Since its peak in April, its price has almost halved in US dollar terms – hardly a convincing store of value.

Bitcoin and similar assets don’t conform to the characteristics of traditional financial assets or currencies. It is difficult to call bitcoin an asset – it has no fundamental economic value other than a very limited role as a medium of exchange.

There are no cash flows and, unlike gold and other precious metals, there is clearly no physical use. It is hard to see how it conforms to being a currency, either. Its lack of uniform legal backing will ultimately limit its use.

It’s no wonder that governments don’t like bitcoin. Economic transactions can take place outside the mainstream fiscal and legal infrastructure. If people are making money through trading bitcoin, there is potential tax to be raised.

Hong Kong and Singapore may have solutions for the world’s bitcoin problem

So far, bitcoin’s real attractiveness has been as a vehicle for speculative trading in a world of excess liquidity, alongside the surge in meme trading. This is very much on the fringe of financial markets, even if some corporations and financial institutions have paid lip service to accepting bitcoin as a viable financial instrument.

Looking ahead, bitcoin might eventually be seen as a trailblazer, however. The technology on which it is founded is paving the way for digital currencies to enter the mainstream and become part of people’s everyday financial life.

04:22

Blockchain in Asia: China’s Ripple Effect

They will also have fundamental implications for banks. By allowing economic agents to settle transactions with a central-bank-administered digital currency, the need for clearing services through the traditional banking system disappears.

A digital HK dollar must not be allowed to undermine the banking sector

Moreover, the role of traditional bank accounts is diminished. Digital currencies would be held within a digital wallet which, for many, would be less costly than a traditional account. Banks will become less of a source of potential financial instability.

There is also a social dimension. For several reasons, some individuals are excluded from holding bank accounts yet still play a legitimate role in the economy. Digital wallets would address the need to have access to a bank payments system.

Isolated rural locations, for example, have often suffered from a lack of access to a “bricks and mortar” bank and would benefit from a cheap, safe and accessible digital currency.

There is also a monetary policy attraction. Central banks have limited control over broad money supply and rely on banks making loans and creating deposits. The incentives of a banks’ credit policies and the needs of the real economy often do not coincide.

A digital monetary vehicle would allow central banks more flexibility in addressing broader monetary policy objectives. Fiscal transfer payments could also be more efficient using digital currencies.

The world is moving away from cash. However, private digital tokens masquerading as financial assets or currencies do not provide the basis for a new monetary system. Instead, digitalising cash and transfers do.

Central bank digital currencies will contribute to an efficient, safe and more equitable financial system in the future. And they don’t harm the environment, either.

Chris Iggo is the chief investment officer for core investments with AXA Investment Managers